Contribution, aka “absolute attribution,” is a commonly used measure of performance. It’s simply the return of whatever we’re evaluating (securities, sectors, etc.) times its weight. We sum these values up, and they should equal the portfolio’s total return, but may not, if transactions have occurred and you failed to compensate for them.

This produces our “winners” and “losers,” often reported as “top 5” and “bottom 5” contributors. One might conclude that if a security is on the “top 5” list that they did well and that having them was a good thing, but not necessarily. Consider the following:

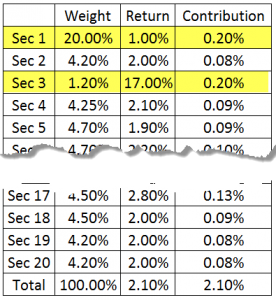

We see that the two main contributors both generated 20 basis points to the total return. One (Security 1) had a return (1.00%) that was significantly below the average and perhaps it was below the benchmark’s average, too. And so, how did it end up being a top contributor? Because of the large weight it has (20%). But is such a weight justified given the low return? Security 3 also generated 20 basis points of contribution, and had the smallest allocation (1.20%), but had the highest return (17.00%).

And so, we see that very large weights or returns can result in large contributions to the overall return. If you were to show these two securities in your “top 5” list, someone may inquire as to why such a (relatively) poor performing stock ended up being a big contributor; the answer is simple: you put a lot of your money there. In retrospect, perhaps you would have preferred to reverse the weights between Securities 1 and 3.

Of course, this is merely a snapshot for one particular period; perhaps over the long term, Security 1 has done extremely well, while 3 hasn’t. But understanding how a security ends up on your “top 5” list is important.