by admin | Feb 3, 2012 | M-squared, Modigliani, risk, risk-adjusted return, Sharpe ratio

In TSG’s January newsletter, I expanded upon a recent blog post where I introduced a couple graphics in an attempt to “make sense out of” negative Sharpe ratios. Two pillars of the investment performance community, Carl Bacon and Steve Campisi,...

by admin | Jan 17, 2012 | GIPS, Global Investment Performance Standards, M-squared, Modigliani, risk

I have been invited to join the CFA Institute’s Jonathan Boersma and Neuberger Berman’s Leah Modigliani to speak on the subject of risk, at an evening event at the NYSSA (New York Society of Security Analysts). The program takes place at 6...

by admin | Jan 14, 2011 | Modigliani, risk

Bruce Feibel, author of Investment Performance Measurement, spoke at the Performance Measurement Forum’s North America chapter’s Fall meeting on the topic of risk. I was quite pleased when he expressed his support for the risk-adjusted measure, M-squared,...

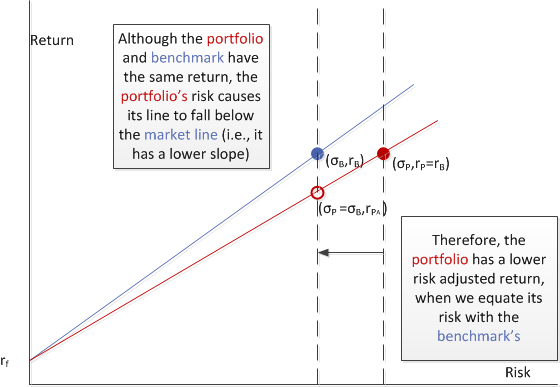

by admin | Jul 23, 2009 | Dietz, M-squared, Modigliani, risk, risk-adjusted return, time-weighting

While I doubt that they were aware of it, when Franco and Leah Modigliani developed their risk-adjusted return measure, M-squared, they were extending an idea first promulgated by Peter Dietz in his 1966 thesis, from which we obtained the notion of time-weighting and...

by TSG | Feb 15, 2007 | GIPS, Modigliani, Performance Perspectives Newsletter, risk adjusted performance measure

VOLUME 4 – ISSUE 6 February 2007 Download PDF...