Some background on the derivation of this fundamental rule of contribution (absolute attribution)

I think it’s worth providing some background into how this fundamental rule for contribution came about.

I’ve been working with a client on their implementation of contribution. During a recent review, I carried out my own analysis and discovered that I was not able to reconcile to the portfolio return. Another fundamental rule is that we should reconcile. But a more forceful one is that when we conduct transaction-based contribution, we must reconcile to the total return: this is the whole point of contribution!

And since I was doing transaction-based contribution, my failure to reconcile meant one thing: there was a problem with my data. But what?

I looked at my table and realized that there was a problem with the cash flows. And what was born was this fundamental rule!

And so, what is this “fundamental rule of contribution (absolute attribution)”

The rule is quite simple: the sum of the sub-portfolio cash flows must equal the sum of the external cash flows.

Simple, right?

To my knowledge, this rule has never previously been declared. And yet, it is fundamental to transaction-based contribution, if we wish to reconcile completely to the portfolio return.

How can we prove-out this fundamental rule?

I think it’s reasonable to consider the cash flows that occur, and why they should, in reality, support this rule.

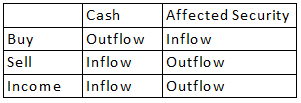

Let’s first consider the internal cash flows. These are, for example, buys, sells, and income.

We have a case of double-entry bookkeeping, which allows us to see these flows essentially sum to zero. Consider the following table:

- A buy requires the transfer of cash (an outflow) to purchase the security, which becomes an inflow.

- A sale results in the removal of shares from the security (an outflow) and the transfer of the proceeds into cash (an inflow).

- Dividends and interest (income) cannot be kept with the security that produced them, but we want that security to get credit for them, so we have an outflow of the income amount from the security, and the transfer of the funds into cash (an inflow).

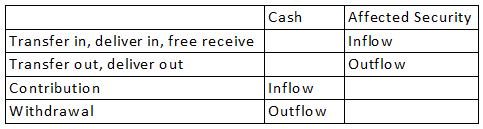

We also need to be concerned with how external cash flows affect sub-portfolios:

Here we have single entry bookkeeping; that is, these flows only affect a single security or cash.

As a result, the sum of these cash flows have to equal the sum of our external cash flows.

A necessary rule to reconcile

If we want to reconcile the sum of our contribution effects to the portfolio return, we must abide by this rule. If you’re finding that you are not able to tie the numbers out, this may be the source of the problem.

Please let me know your thoughts on this. I’ll be addressing the topic in greater detail in this month’s newsletter.