At this year’s annual #GIPS conference, we learned that the GIPS® Executive Committee is beginning work on the next edition of the Global Investment Performance Standards: GIPS 2020, or as those of us who Tweet will probably refer to it, #GIPS2020.

While exercising this morning I thought that perhaps it’s a good time for us to come up with a “wish list” for these Standards. The last edition was in 2010, and talk has it that #GIPS2020 will see some significant changes. And so, why not ask for a few things? Well, here’s my initial list.

#GIPS2020 Wish List Item #1

One of the most confusing things about GIPS, and there are a few contenders, is the use of the word “discretionary.” The original drafters of these Standards, for some unknown reason, decided to use a word that was already well entrenched within the investment lexicon. (It was probably because the AIMR-PPS® had borrowed this word, so GIPS just continued with the practice.)

Clients grant their brokers or investment managers the discretion to trade on their behalf. BUT THAT IS NOT WHAT GIPS MEANS by “discretion”!!! In “GIPS speak,” when we hear or read “all actual, fee paying, discretionary accounts” we are speaking of the account being representative of the strategy.

I say it’s HIGH TIME to replace “discretionary” with “representative.” What will it cost us? ZIP!

We changed “market pricing” to “fair value pricing.” Why not make this change? What possible reason can we have to continue to use a word that confuses just about everyone, even many who’ve worked with the Standards for years!

#GIPS2020 Wish List Item #2

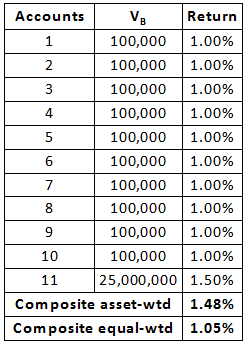

Change the composite return from asset- to equal-weighting. Why? Well, consider this scenario:

GIPS mandates the use of asset-weighting for the composite return. In this case, it’s quite evident that the largest account skews that return quite a bit. You might suggest that this never happens, but I can assure you that as a verifier I have seen this, and worse, where the composite’s return IS the return of the largest account, meaning the other accounts had no influence whatsoever on the composite return. This situation often happens when a firm includes a mutual fund with separate accounts, and that mutual fund is quite large relative to the other accounts. It also happens when there are one or two very large accounts that dominate the weighting. Granted, the difference might not be 50 basis points, but in the end, the largest account(s) decides what the composite’s return will be.

Back in the early 1990s, as the AIMR-PPS was being finalized, two groups, the ICAA (Investment Counsel Association of America, now the IAA) and IMCA (Investment Management Consultants Association) lobbied the Association for Investment Management & Research (what the CFA Institute used to be called) to use equal-weighting. But, those on the AIMR-PPS working group wouldn’t relent from their plan to use asset-weighting.

I recall reading a paper from the ICAA that argued with asset-weighting, the manager could favor the largest accounts, since they’d know that these would have the greatest contributing affect on performance. IMCA was so opposed that they created their own standard; granted, it didn’t succeed, but it still was their statement that asset-weighting was wrong. But the AIMR-PPS apparently wanted asset weighting because it would be as if the composite was a single account.

But Why?

At the time I’ll confess that I really didn’t have an opinion on this. But today, especially after working with the collective standards for nearly 25 years, I’ve become a huge fan of equal-weighting.

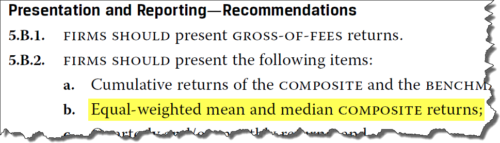

Okay, the Standards do recommend the use of equal-weighting, it’s true.

But NO ONE does this. And why not? Probably two reasons:

- First, there are plenty of columns already on the composite presentation, why add another?

- Second, why add to the workload if there’s not a perceived benefit?

The Standards already ask for plenty; no need to add additional items.

A manager doesn’t manage a composite nor do they invest the composite’s collective assets; rather, they manage individual accounts and invest each account’s money. When a prospect is looking at a composite presentation, don’t they want to know what the average experience was of the managed accounts?

- The asset-weighted return isn’t that.

- The equal-weighted return is.

And, it seems like a perfect time to make the switch.

I’d simply have something like “effective 1 January 2021, composite returns must be equal-weighted.” And while I’d recommend retroactive adoption, I wouldn’t require it.

Simple. Effective. Easy. And, MUCH BETTER!

#GIPS2020 Wish List Item #3

Anyone who’s read this blog or our newsletter knows of my fondness for (actually, appreciation of) the internal rate of return. But to clarify, I don’t dislike time-weighting: I find time-weighting to be an exceptional way to evaluate the performance of managers who do not control cash flows. BUT, for just about everything else, we should use money-weighting!

GIPS today requires its use in very limited situations (e.g., closed end private equity funds). The rule, however, should be quite simple:

Require the IRR whenever the manager controls the cash flows.

When you’re told that the IRR is used because of the illiquidity of the investment, please disregard it. Yes, the liquidity can be a factor, but it clearly isn’t the sole or even major factor. The real issue is control of the cash flows. Why make the rules complex?

This is SO VERY SIMPLE.

There is a subcommittee that is apparently looking into expanding the role of the IRR. HOPEFULLY they’ll be open to this suggestion.

#GIPS2020 Wish List … what else?

I’m sure you can think of things you’d propose. And so, why not?

I will write a formal letter to the GIPS Executive Committee detailing these items and others.

We can expect that they will release a draft of #GIPS2020 for public comment at some point around 2020, perhaps in 2019. You should review that document and comment. But why not let them know how you feel about a few things? They seem to be open to wanting to hear from us, so let’s tell them what we think? And, if you disagree with me, you’re obviously welcome to tell me and them.

The GIPS EC’s #GIPS Survey is waiting to hear from you!

The GIPS EC is looking for comments. As I mentioned in a recent blog post, they’d like you to participate in a VERY brief survey. I’m just looking to extend this drafting of “wish list items” to provide even greater attention to the opportunities and possibilities to improve GIPS.